Capitalism – The Good and Bad

Capitalism, an economic system in which private owners rather than the state control a country’s trade and industry, has been the principal driver of American economic growth. It’s brought the benefits of a higher standard of living to most levels of society in the United States and throughout the world. But the path that allowed ordinary people to climb to economic prosperity isn’t what it once was. I’m not referring to the work of evil doers, like pharmaceutical companies that knowingly pushed shipments of opioids into communities far beyond their medically acceptable needs. Or tech companies that permitted (and still permit) the distribution of false information, misinformation or disinformation. No, it doesn’t take something so dramatic. There are far more insidious means of promoting and institutionalizing corporate greed, and they are a divisive force, exacerbating income inequality and diminishing funding for government services. Another example of capitalism run amuck.

Growing Up With Capitalism

My first exposure to capitalism probably occurred some seventy-five years ago when I set up a lemonade stand to buttress my weekly allowance. I sold lots of lemonade, and felt pretty successful. When I got older, I became aware that hard work and taking calculated risks could be rewarding. Entering the professional work force as an accountant with, at the time, one of the “Big Eight” accounting firms, I saw first-hand the inner workings of a variety of manufacturing, retail and extractive industries. Perhaps I was somewhat naïve and idealistic, but I believed an unwritten compact existed between the company, employees and community. Companies invested in a community and its workers, and reaped the benefit of their loyalty. That does not mean there were no conflicts. History of the labor movement is replete with them.

Globalization

Then there was the movement to globalization, which initiated the substantial dissolution of this compact. It came first in manufacturing, followed by significant innovations in automation that magnified its impact throughout the economy. A rabid socialist might object on ideological grounds when a company abandons a U.S. facility and moves its operations overseas. However, a dispassionate analysis refutes that assertion. Lower priced products of comparable quality flooding the U.S. market put U.S. companies at a competitive disadvantage. And if a company can’t remain competitive, it couldn’t remain in business. A failing business was also not so good for its employees and community. That is, unless there was a “rich daddy” willing to sustain an unprofitable business.

Perhaps one could argue that the U.S. should not have opened its market and imported lower priced goods. That prompted U.S. companies to move to lower cost markets and the loss of U.S. manufacturing jobs. But the fact is that while manufacturing jobs were lost, the U.S. consumer benefited greatly by lower priced goods. And the countries that produced them were able to raise their standards of living.

Nevertheless, I believe not enough was done to help the then soon to be dismissed employees in terms of the amount and length of severance pay, and most importantly, their retraining. In many respects, I place the blame for that on the federal government. I’ve always believed that there should have been legislation addressing this issue, either in the form of an “exit tax” charged to the departing company, or a tariff for a limited period on its goods coming back to the U.S.

Automation

Automation presents a similar situation: technology has allowed companies to reduce their labor force. This does not impact only manufacturing where machines replace men who previously performed certain jobs. Think retail, where optical scanners reduce the cashier’s time required to check out a purchase. Then there are self-checkout machines that eliminate the need for a cashier at all! Toll plazas use scanning machines to assess and effectively collect tolls.

Soon we will face a changing environment as we exit the Covid-19 pandemic. Some companies will likely reduce their presence in fixed office space. That could have a domino effect, reducing the number of employees required to clean and maintain them. It should be clear that for a company to remain in business, it must control its costs. Inevitably that could result in reduced employment. Thus, there is ample justification when companies reduce their labor force to remain competitive. And when I say “companies,” I mean that interchangeably with “corporations.”

Sources of Government Revenue

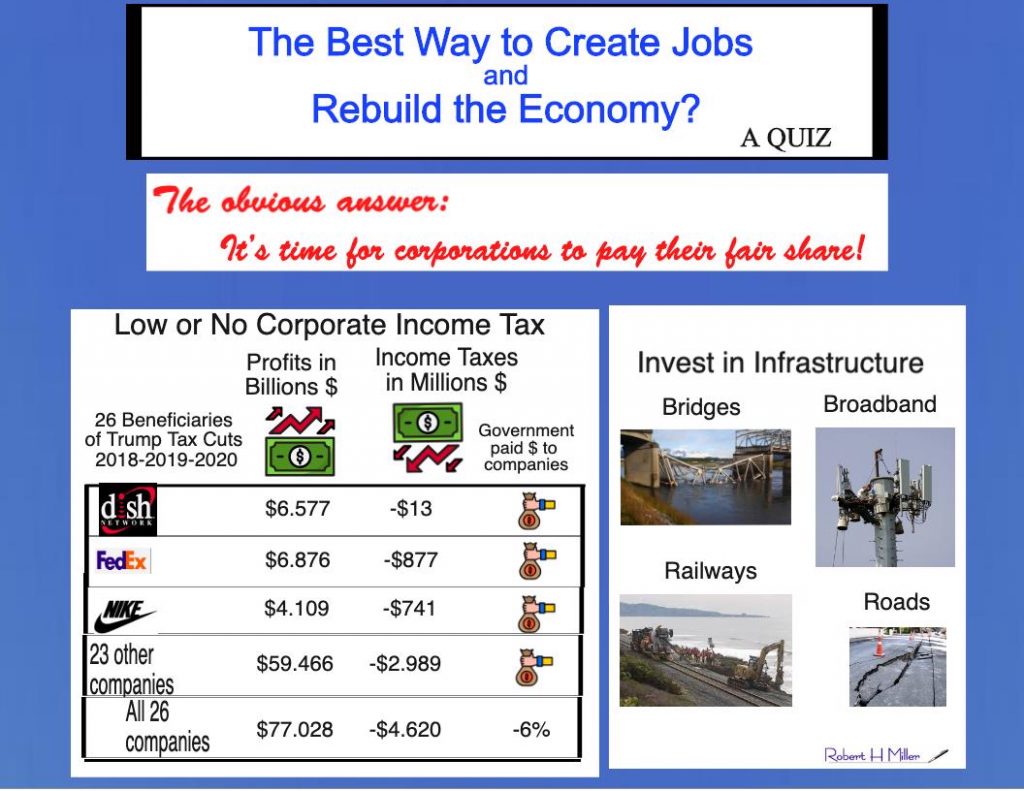

But now let’s look at the other side of the ledger. Let’s see how corporations have forsaken their responsibilities to the country that provides the prosperity they enjoy. And, of course, most significantly, let’s begin with the relatively low amount of taxes corporations pay. Or in the case of several large profitable corporations, don’t pay any at all.

The federal government obtains its revenue from these sources: individual income taxes, corporate income taxes, social insurance and retirement receipts, and excise taxes and other taxes.

In 2019 individual income taxes accounted for 49.6% of government revenue and corporate income taxes 6.6%. Corporate income taxes were not always this small a percentage. After the Second World War, the share of federal government revenue from corporate income taxes dropped from the mid 30% range to the mid 20% where they remained until 1967. Since then, they’ve been hovering in the single digits, occasionally rising to 10%+. This has had a particularly negative impact on funding government operations, exacerbating the annual budget deficit and debt to finance it.

The Fallacy of Low Taxes and Economic Growth

Corporations and their conservative supporters argue that lower taxes are necessary to remain competitive with foreign companies, support job creation and grow the economy. Republicans used that argument in passing the 2017 $1.5 trillion tax cut. They claimed lower tax rates would create economic growth that would pay for the resulting loss in revenue. Objective economists scoffed at this assertion. It was based on “supply-side economics,” a theory that has been consistently discredited for decades. Time has proven them right as the Trump tax cuts have not delivered as promised.

As someone who joined in the chorus of naysayers in 2017, I should also point to a research study of taxes and job creation in 2012, published under the title If Low Taxes Create Jobs, Where Are They? Utilizing empirical data, I demonstrated, unequivocally, that there is no correlation between low taxes and job creation. In fact, historically, more jobs have been created at higher rather than lower rates.

The argument that U.S. income tax rates must remain competitive with those of other countries has merit. But by itself, avoids fundamental issues relating to international business. First, as investments are concerned, a country’s income tax rate will ordinarily not be the defining issue. Local economic and political environment, labor, other costs and workforce quality will more likely tip the scales in that decision. Additionally, focus on income tax rates ignores the social taxes many developed countries have that are higher than the U.S. Taken together with social taxes, U.S. corporate income tax rates pre-Trump 2017 cuts were competitive with those in other countries.

Changes Required in Taxation of Corporations

So, let’s cut to the chase. U.S. corporations should be paying more to fund the government that provides the opportunity for them to operate profitably. And certainly, there is no justification for corporations to report billion(s) of dollars in profit yet pay little or no income tax. In my Blogs noted above and that of May 2019, I outlined the many ways a corporation can avoid taxes by shifting profits to lower income tax rate countries, and how U.S. tax law should be changed to prevent that. I will not repeat my analysis here. Suffice to say, legal tax avoidance schemes not based on real economic rationale should be, and must be eliminated. Additionally, there must be a minimum tax based on a corporation’s reported “book income,” which generally drives the company’s progress.

Ideally, the sum of the book profit of all the corporation’s U.S. based entities would be the basis for U.S. minimum income tax calculations. However, this may not be readily determinable or even reliable. To avoid any complexity, I would recommend that the percentage of U.S. source revenue to a corporation’s reported worldwide consolidated revenue be applied to consolidated book income to arrive at U.S. taxable income, and a minimum tax rate be applied to that amount. That revenue is an appropriate basis for ascertaining profitability since it is more accurate than related costs, which are, at best, estimates or, at worst, manipulated. It is certainly a reasonable expectation that corporations pay a fairer share of the cost of government operations.

A Rising Tide Doesn’t Lift All Boats

It is often said that a rising tide raises all boats. And in the past, as the standard of living rose, one could assert with confidence that the spread of capitalism throughout the United States was an energizing force. Many individuals benefited from the capitalistic economy and built enormous personal wealth. But just as with corporations, the exercise of capitalism within the existing tax structure, exacerbating income inequality is detrimental to society. Here’s why.

Studies have shown that income inequality depresses economic growth by decreasing per capita income, damaging health and well-being, decreasing disposable income, or individuals incurring debts they’re unable to pay. “In 2014 the Organization for Economic Co-operation and Development, a collective of the world’s 35 wealthiest countries including the United States, found that rising inequality in the United States from 1990 to 2010 knocked about five percentage points off cumulative GDP per capita over that period. Similar effects were seen in other rich countries.”

A major factor perpetuating rising inequality is current U.S. tax law allowing much of that wealth to accumulate tax free. That is not to say the wealthy do not pay income tax. In fact: “The latest government data show that in 2018, the top 1% of income earners—those who earned more than $540,000—earned 21% of all U.S. income while paying 40% of all federal income taxes. The top 10% earned 48% of the income and paid 71% of federal income taxes.”

Changes Required in Taxation of Untaxed Accumulated Wealth

So, the issue is not that the wealthy don’t pay income tax. As the above statistics show, high income individuals pay the majority of income taxes. The issue relates to those wealthy individuals who accumulate their vast wealth while earning very little in salary. Income from salary is subject to ordinary income tax rates while investments in real estate, stocks, art and other assets are not taxed until sold and then at much lower capital gains rates. The existing 3.8% Net Investment Income Tax relates to annual investment earnings. It does not address the issue of untaxed appreciation in wealth. Additionally, much of that wealth can also be passed on to future generations untaxed. Thus, higher income tax rates on the wealthy’s income, alone, will not solve the problem of widening economic inequality.

It is in the country’s interest to mitigate income inequality, and that will require significant changes in U.S. tax law. Fundamentally, it must tax existing untaxed wealth and preclude the untaxed accumulation of wealth in the future. One method is a tax on high-net-worth individuals, estates and trusts beyond the existing Net Investment Income Tax of 3.8%. For example, individuals, estates and trusts with a net worth of at least $100 million should file an annual statement of net worth with the IRS based on “Generally Accepted Accounting Principles.” Tax rates could be progressive but structured with specific tax amounts within each bracket, for example: $100 million – $250 million – $500 million – $1 billion – $2 billion – $5 billion; over $5 billion.

Accumulated wealth in private foundations and endowment funds at private universities and colleges is another source of untaxed revenue beyond the 1.4% excise Tax on Net Investment Income. Here too, appreciated wealth remains untaxed until realized.

Danger Ahead in Growing Deficits and Debt

Our country has significant problems funding programs that benefit all Americans, among them rebuilding infrastructure, providing adequate healthcare and addressing climate change. Congress has essentially ignored these issues for several decades while focusing on continually lowering tax rates with little regard to the annual deficit or accelerating debt. This cannot go on indefinitely. As a country that prints its own currency, which is also the world’s reserve currency, we have a way to go before we’re unable to borrow enough to keep the ship afloat.

When individuals spend more than they earn, their debt increases as does the interest paid each year to finance their growing debt. Eventually the amount spent on interest precludes spending on other necessities. Though the government’s budget is unlike that of the average individual, accelerating debt requires an equal acceleration in its funding. That can lead to a higher cost of borrowing if lenders demand a larger return on what they perceive to be a greater risk. The result is an increase in interest expense due to both the volume of debt and the rate of interest paid. It can also stimulate higher prices as inflation takes hold. Thus, even with government, the amount spent on interest will ultimately overwhelm spending on other obligations.

The Need For Action – Now!

We can no longer ignore this issue. It is now time for action. We must increase government revenue, and the best way to do that is to tap those beneficiaries of government largesse who have paid little or no tax on their reported profits or appreciation of their wealth. That means corporations and high net worth individuals, estates, trusts, endowment funds and private foundations with untaxed accumulated wealth.

Some may consider a tax on net worth too radical and a step too far on the road to socialism. If the new tax rates are confiscatory, then I would agree. But I do not believe small percentages, such as a 2% tax on balances of $100 million or even $1 billion are confiscatory. And, if the net worth declines from one year to the next, the current year’s tax base could be reduced by that amount. So, in that case, every two years, the tax would be based on the same net worth amount. Additionally, the current year’s earnings would be excluded from the net worth calculation. Yes, this places a greater burden on the wealthy, but is it really too big a price to pay?

To be clear, I am a capitalist and always have been and will be. But I’m also objective enough to recognize when something is wrong and needs to change. Even if that change requires a radical departure from what we’re accustomed to.